“There is more than £25 billion outstanding in unresolved tax bills and it is essential that there should be proper accountability to Parliament for the settlements reached by HMRC.”

Margaret Hodge MP – Chair, Public Accounts Committee, 20 December 2011

“HMRC rejects the conclusion of the PAC that there are systemic failures in the management of tax disputes. The report is based on partial information, inaccurate opinion and some misunderstanding of facts”

HM Revenue and Customs, 20 December 2011

Today a row erupted between the Public Accounts Committee (PAC) and HM Revenue and Customs (HMRC) over issues of outstanding taxes.

The controversy followed the publication of a PAC report in which it cited potentially £25.5 billion of tax at stake from over 2,700 issues between HMRC and the “biggest companies”.

The potential costs were prominently reported in the media:

The Times: “Taxman taken to task over uncollected £25bn debts”

Daily Mirror: “BRITAIN’s top taxman was today attacked for failing to collect £25billion of revenue and letting big companies off paying their bills in full.”

The Sun: “Firms’ £25bn tax let-offs”

Given the widespread coverage of the issue, Full Fact decided to investigate the source of the dispute.

Analysis

Given the large amount of coverage of the dispute, readers might be led into believing some of the headline figures have just been ‘revealed’ by the Public Accounts Committee investigation.

In fact, the figure of £25 billion was published back in July this year, andreported by the Financial Times.

The figures for unresolved tax disputes emanate from a report by the Comptroller Auditor General from the National Audit Office (NAO), which examines the accounts of HMRC.

Referring to the resolution of tax disputes, the report states:

“At 31 March 2011, the Department was investigating over 2,700 issues with the largest companies, with potential tax at stake of £25.5 billion.”

It is worth noting at this stage that the NAO’s figures are based on financial years up to 2010-11, and hence the figure of £25.5 billion reported today is already eight months out of date, and could be higher or lower in reality.

The first point of clarity provided by the document is what is meant by “biggest companies” when commentators have described the supposed beneficiaries of the unresolved issues.

The figures concern, specifically, the 770 largest companies who are dealt with by the HMRC ‘Large Business Service’.

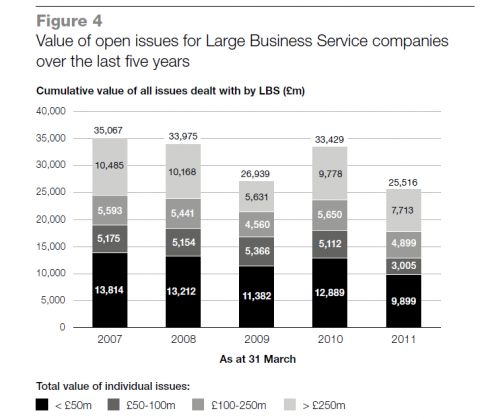

Since the value of each company’s ‘issue’ with HMRC varied considerably, the NAO provided a breakdown of the unresolved issues:

The chart above verifies a total estimated value of the outstanding issues of £25,516 million as at 31 March 2011, down from an estimated £33,429 million as at 31 March 2010.

As the notes to the chart note, this is not necessarily a representation of the number of new disputes each year, but the total outstanding. Hence, some issues could carry over multiple financial years.

So far, so good for the Public Accounts Committee’s appraisal. However, the HMRC provided Full Fact with details of why they disputed the PAC’s claims. In a statement, a HMRC spokesperson said:

“We explained to the Committee and again in a letter to the Committee Chair in November that this figure [£25.5 billion] is a ballpark estimate of maximum potential tax liabilities, before a full investigation of the specific facts has taken place, and before applying any reliefs or allowances that would normally be due.

It is not actual tax either owed or unpaid. In many cases, when HMRC has looked at the full facts it becomes clear that there is no further liability at all. Tax under consideration is an administrative tool to help us to focus our resources on cases where potential tax liabilities appear to be greatest. It is not tax owed.”

The NAO’s notes also seem to support HMRC’s concerns. They make clear that the taxes involved in the issues are estimates “before any consideration of the facts has taken place and before any reliefs or allowances are applied.”

Crucially, they state: “it does not represent tax owed or unpaid”.

HMRC were unable to provide specific examples of what may constitute ‘reliefs’ or ‘allowances’. However, there is extensive Government informationon the possible means of claiming these, such as Capital Allowances which allow companies to claim on new assets acquired.

Full Fact contacted the Committee for a direct response to the caveats pointed out by the HMRC, but they were unable to comment ahead of a formal response by the Treasury.

Conclusion

A closer look at the figures behind today’s headlines reveals a number of caveats ill-reported by elements of the media.

The NAO statistics make explicit that the estimates for outstanding tax issues do not take account of, beyond case-specific issues, any due reliefs or allowances to companies involved in the disputes. Hence, in some cases, the eventual tax repayment could be far lower that the estimates imply.

This poses a significant problem for newspapers who simplified the issue in their reports. The Times and the Mirror refer to “debts” and “uncollected tax” in their reports, terms which fail to capture the reality of the disputes between HMRC and the companies involved.

Nevertheless, questions remain regarding the arguments employed by both the PAC and HMRC. Margaret Hodge’s statement in the press release from the PAC fails to acknowledge the caveats of the available data, and the PAC report itself provides only a source link to the NAO while failing to emphasise the nature of the estimate.

Meanwhile the HMRC’s dismissal of the PAC’s report as being based on “partial information”, “inaccurate opinion” and “misunderstanding of the facts” is not satisfactorily explained by the dispute over this figure alone.

While the background to the £25.5 billion figure is more clear, it remains to be seen what other details the HMRC takes exception to.

Our Tax Disputes professionals are available to give information and advice. To contact one of our specialist Lawyers please click here or call 02071830529.